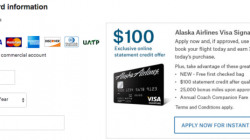

During Alaska Airlines’ recent quarterly earnings call, Chief Commercial Officer Andrew Harrison discussed the popular Alaska Airlines Visa Signature Card and the company’s plans to make it even better. Among the key enhancements is a new sign-up bonus of 30,000 miles effective June 1. (Hat Tip to Wandering Aramean)

Alaska has historically offered just 25,000 miles, which pales in comparison to the 50,000-mile offers for some other airline cards. But realize that many of those competitors are now also offering just 30,000 miles, with only targeted customers getting more. The new sign-up bonus will put Alaska on a more even footing.

I think more miles are great. My concern is that Alaska Airlines doesn’t quite understand what makes a great credit card earn a permanent spot in my wallet.

Bigger One-time Bonus? That’s It?

From the earnings call transcript:

We expect our growth in card members to remain strong because come June 1, we’ll be able to go to market with new cardholder products we negotiated with our new agreement and includes a 30,000 bonus miles on approval that’s an increase of 20% from today and a free bag. In addition, new and existing members will no longer incur international transaction fees. We believe that this is the best airline credit card offering in the market, bar none.

So, Alaska Airlines believes that their Visa Signature Card will be the best airline credit card on the market as of June 1. With just these three benefits, I think that would be difficult to defend, but there are other perks like the $99 annual companion fare that aren’t mentioned here and would probably stick around. That helps tremendously. Used wisely, every companion fare has saved me $300 to $700 per year on tickets in coach (not accounting for the ability to upgrade these tickets using my MVP Gold Guest Upgrades).

But a free checked bag is already a new benefit and is irrelevant to most frequent flyers. No foreign transaction fees aren’t in effect yet but were leaked at the brand unveiling in January. And they save maybe 2-3% on a few thousand dollars in purchases each year? Most people are not spending half their time outside the country.

I think the focus is on the sign-up bonus, and that makes me ask: Was the Alaska Airlines credit card not great before? Is increasing the bonus by only 5,000 miles enough to go from worst to first? I don’t believe it was the worst, but how much has really changed here?

The Problem Is Ongoing Bonus Categories

Ultimately banks and their co-brand partners want their credit card to be in your wallet all the time so you’ll be more likely to use it for everyday purchases. Increasing the sign-up bonus is a new reason to get the card. The companion fare is a reason to keep the card. What is my reason to use the card?

To be a truly competitive card and earn a permanent place in my wallet, the Alaska Airlines Visa Signature Card needs to offer bonus spend in categories other than Alaska Airlines flights. Consider that nearly all flights are booked at home. I can keep my card in a drawer and pull it out when I book a flight, then put it away. I get the companion fare whether I take it out of the drawer or not. The rest of the time it’s just a 1X card.

Next to airfare, my two biggest regular expenses are hotels and groceries. Many airline credit cards offer 2X miles on hotel transactions, but Alaska doesn’t — and if they have plans to do so then they haven’t told me. I would gladly carry that card with me to pay for hotel stays as I think 2 Alaska Airlines miles are worth more than 2 Ultimate Rewards points from the Chase Sapphire Preferred or Chase Ink Plus. Even so, some hotel purchases are pre-paid.

A bonus on grocery stores (or dining) would keep that card in my wallet all the time. The only reason I keep my American Express Premier Rewards Gold Card in my wallet is because of the 2X grocery bonus. Other than that I have the same complaints as I do about Alaska’s card — I like the bonus on airline purchases but can easily keep my Amex in a drawer, pulling it out only when needed.

Conclusion

Ultimately I don’t think Alaska Airlines has a problem with making their credit card attractive to get and keep. The question is how they encourage people to use it and make it a daily part of their spending habits. Within the Pacific Northwest, I see many people use their Alaska Airlines credit card as a mark of local pride. That only goes so far. Matching the bonus categories offered by other airlines, or coming up with new ones, is what they really need to sell the claim that theirs is the “best airline credit card.”