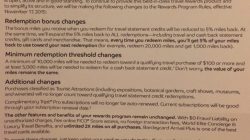

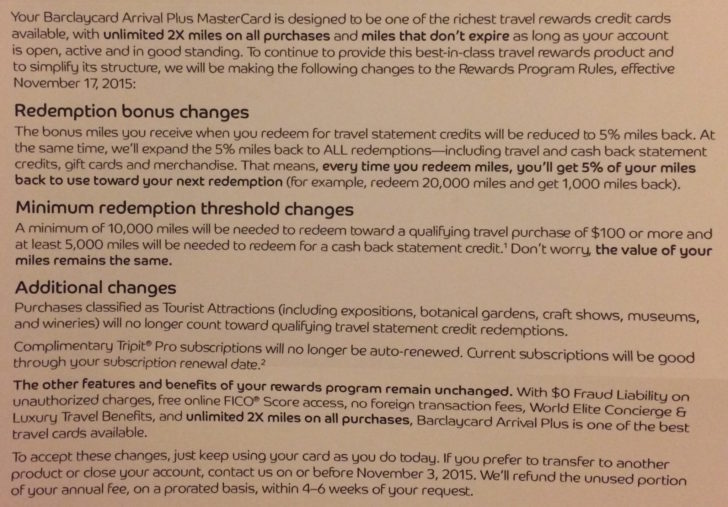

Earlier this month, I detailed the changes coming to the Barclaycard Arrival Plus Mastercard. While none of the individual changes are terrible, together they really devalue the overall value of using the card. To review, the changes are:

- A 5% rebate on all redemptions, down from a 10% rebate only on travel redemptions. The educated readers of the miles/points blogosphere know to use Arrival miles only on travel redemptions, so this brings the card down from a 2.2% back card to a 2.1% back card.

- An minimum 10,000 Arrival miles needed for redemption, meaning only purchases of $100 or more count.

- Tourist Attractions are no longer eligible for travel statement credits.

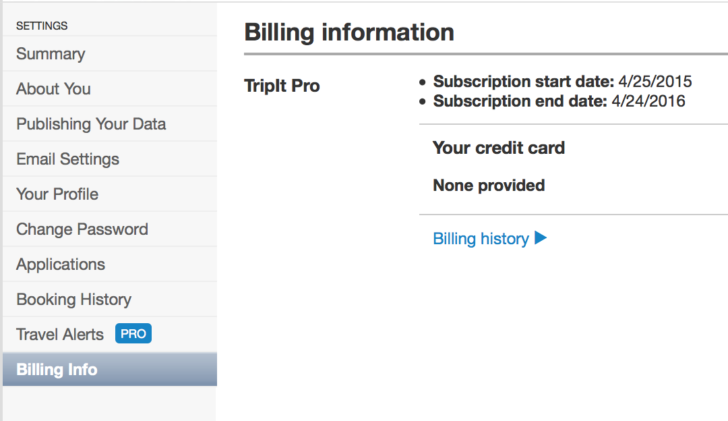

- TripIt Pro subscriptions are no longer offered. Current subscriptions are valid through their expiration date. You can log in to your TripIt account, click the “Settings” options under your name in the upper right hand corner, and check billing info to see when your TripIt subscription is good until.

I haven’t checked my mail, but reader Ben was kind enough to send me a letter he received from Barclays as a current Arrival Plus cardmember.

Current Cardmembers Have Until November 3rd To Enjoy Current Benefits Before Downgrading Your Card

At the top of the letter, it says that the new Rewards Program Rules are effective starting November 17th. That means that you’ll still get a 10% rebate on miles and be able to redeem for travel charges between $25 and $99.99.

However, at the bottom of the letter, Barclaycard states that current cardmembers have until November 3rd to either change or close the card and receive a pro-rated refund of any annual fee you paid.

My annual fee posted in late April, so my plan is to use my Barclaycard Arrival Plus as usual and redeem all my points by late October. For this purpose, things like airline or hotel gift cards for $25 would be a great buy. If I plan my purchases and point redemptions wisely, I’ll only be left with 250 points after a final 2,500-point redemption, but I should get around $44.50 back to my annual fee.

Instead of canceling the card, my plan is to downgrade it to the Arrival non-Plus, which has no annual fee. I value the credit history this card provides as well as the credit line.

The Arrival Plus is still a good card to sign up for. Just not to hold onto.

The reason I had the Arrival Plus as a primary card was because it provided value even after I finished the signup bonus. It was a great card to spend on – despite the $89 annual fee, 2.2% back toward travel is fantastic; that extra 0.2% made the card worth it if you spent enough on the card. It was also a great card for benefits – the TripIt Pro subscription was useful, and it still has proper Chip+Pin functionality when abroad.

The one thing that’s not changing is the signup bonus – it’s still 40,000 points after you spend $3,000 within 90 days. With the rebate going down from 10% to 5%, the value of those points goes down ~$20, but it’s still a great bonus for the amount of spending you have to do.

And it’s still a decent card for the first year – the annual fee is waived and you’re still earning 2.1% back on your spending, which beats a 2% cash back card. However, the long-term value of the card is shot, and I would highly debate keeping it once the second year annual fee hits.