A couple readers have asked me lately to give some advice on how applying for multiple cards will affect their credit scores. Keep in mind that I don’t have any special insight into how the credit bureaus like Experian, Equifax, and Transunion design their algorithms, but we can deduce some consequences based on the information they provide about relevant factors.

The advice I present can be helpful both before and after a new card application, but really it’s about maintaining a good score all year long. Each new application docks your score about 2-5 points in addition to the factors mentioned below. And while the fact you applied will stay on your record for two years, the effect on your score should wear off in a few months.

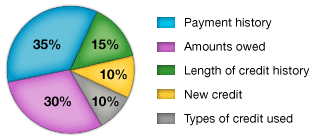

Average Account Age

A person’s average account age gives credit bureaus some information about your ability to maintain a long-term history with a bank while paying your bills on time and being a responsible user of financial credit.

If you one account open for 30 years and then open a new account, your average account age will drop in half to 15 years. This sounds like a horrible thing, but it’s more of an absolute factor than a relative one in my experience.

My average account age, for example, is just over 2 years, yet I have a credit score of roughly 800. I have a few cards that have been open for many years, but most are usually those I signed up for just to receive the bonus. The latter rarely last a full year and get replaced with each new batch of cancellations and applications. It would be wise to apply for one or more no-fee cards like the Chase Freedom card as soon as possible. Even if you don’t use them, you can lock them away and grow your average account age.

If you plan to apply for new cards soon and are thinking about closing an existing card, keep in mind that CreditKarma only reports an average age using accounts that are currently open. Your credit report will include closed accounts, as well, for up to 10 years after the account was closed. A large number of short-lived accounts could hurt you, though it doesn’t necessarily mean you won’t get approved on a new application. This is where you can rely on the discretion of a credit analyst by calling a bank’s reconsideration line.

Credit Utilization Ratio

This is one factor that trips up people the most often in my experience, and it has definitely stung me before. Credit bureaus — and banks — are concerned about how much of your existing credit you are using. They calculate this number for each individual card AND for your available credit across all accounts.

If you have 8 cards with a $10,000 limit on each and have focused your spending on a single card, you may have a $9,000 balance at the end of the month. Your average credit utilization is 11.25%, but your utilization on that one card is 90%. Not good. You should try to keep both numbers under 30%.

I am not certain how frequently these numbers are updated with the credit bureaus, but I would feel confident betting that this happens at least once a month with each account statement. It might be good to pre-pay your cards a month before new applications to bring down your credit utilization. You can also try shifting your available credit between cards at the same bank (super easy at Chase) or request additional credit on an existing card.

Something else to consider is how certain cards are reported to the credit bureaus. Business cards are reported separately and do not appear on your personal credit report even though your personal report may be evaluated during the application.

Charge cards, which must be paid in full each month, sometimes make claims about “no pre-set spending limit.” It’s really a secret limit they don’t tell you, and the limit reported to credit bureaus is often not a limit per se but the highest account balance you’ve had since the card was opened.

So if you consistently charge $1,000 per month, then your implied “limit” will be $1,000. I suggest finding an excuse at some convenient time to spend oodles of money on your charge card(s), but only if you know you can pay it off at the end of the month. Long vacations, weddings, and jewelry are all good ideas.

Number and Diversity of Accounts

Having more credit from more banks is a good thing most of the time. It means the banks trusted you with credit before, you haven’t screwed up, and so it’s probably safe for them to trust you with even more.

So I wouldn’t worry about adding more accounts. If anything it might help. But one thing you can do to improve your chances for future applications is to diversify the types of accounts that you have open.

My credit score is probably near a ceiling because I don’t have a mortgage, a car loan, or a student loan. Megan does have a student loan and has consistently had a better credit score than I do despite similar behavior. When I used to have a car loan, my score was slightly higher than it is now.

I do have a charge card, which is technically a different form of credit than a credit card since it must be paid off each month. It’s an easy way to improve in this category. It may not make much economic sense to open a car or home loan just to raise your credit score, but I’m suggesting that it is one thing that might help you if the opportunity is available and other factors are already pointing you in that direction.

So What’s the Best Way to Raise Your Credit Score?

There really aren’t any secrets here. Having and using credit well makes banks willing to give you more credit. But you never want to look like you need credit, which is why a recent application will hurt your chances when applying for two cards in short succession. A bank determines these things using a variety of metrics like credit utilization and account age. The act of closing cards before a new application doesn’t hurt or help you per se but can affect other metrics that are important to your credit score. Applying for a new card does hurt you, just by itself, though the impact is short-term.

My advice if you are planning to apply for one or more new cards is to (1) pay off your balances and shift spending to reduce your credit utilization ratios in total and separately, (2) make sure others do the same if you’re listed as an authorized user on their accounts, (3) wait.

Waiting is the best thing you can do. Wait at least a month for updated information to be reported to the credit bureaus. Wait at least three months after applications for new credit (though less is probably fine if you have very few applications in the past two years). I personally wait four to six months between new rounds of applications to avoid looking like a hard-core churner, though I’m sure my file still raises some eyebrows.