The process of writing a Devil’s Advocate column consists of three painstaking steps. Step One is coming up with an idea. Step Two is writing it. And Step Three is consuming enough gin to make it through Steps One and Two.

That’s why I love Twitter, because people often tweet suggestions at me for Devil’s Advocate topics, which saves me the trouble of having to go through Step One. Of course, it’d be nice if those people would also write up the post as well. Then I could spend all week completely focused on Step Three, which I think we all agree is what I’m best at.

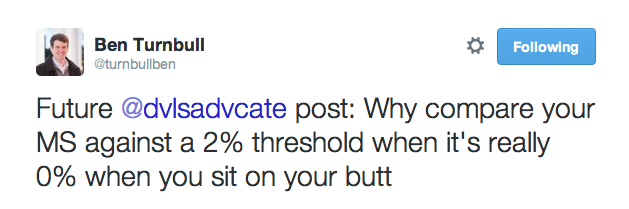

But I’m still appreciative of those who provide ideas, and today’s column is a perfect example. A few weeks ago, Ben Turnbull, a follower and follow-ee of mine who always has intriguing comments on Twitter, sent me the following tweet:

I immediately thought Ben had brought up an interesting question. Conventional Wisdom says we should use a baseline of 2% when considering the rewards on our credit card spend. But Ben points out we’d get 0% by doing nothing, so why isn’t that our starting point? Shouldn’t we consider any net return a bonus?

There’s logic behind the Conventional Wisdom, but I think there’s some validity to Ben’s idea as well. So let’s pour ourselves a fresh glass of Step Three and take a look at it from the Devil’s Advocate point of view.

What’s up with this 2% in the first place?

For readers who might not have heard of the 2% theory, here’s the idea: since we can get 2% cash back on all our credit card spend by using a card such as the Fidelity Investment Rewards Amex or the Citi Double Cash card, we should consider that the minimum reward rate. So if we instead choose to collect miles or points in a loyalty program such as Ultimate Rewards or American AAdvantage by using their credit card instead, we need to realize we’re “giving up” 2% cash back in lieu of those proprietary points.

That means any return from those points had better be at least 2% and probably more, given that we’re also forgoing the flexibility of cash for a harder-to-redeem points currency.

Now, keep in mind that 2% cash back cards don’t have any bonus categories, while many other rewards cards do. If you’re getting 2x points on dining and travel with a Chase Sapphire Preferred, and if Ultimate Rewards points are worth more than 1 cent apiece (which they are, since you can redeem them for at least 1.25 cents per point directly against any airfare without restriction), you can definitely do better than 2% with certain rewards cards in the right categories.

But that calculation still uses 2% as a baseline — it just demonstrates we can in fact do better than 2% even with a rewards program. What it doesn’t show is whether we should be using 2% as a guideline in the first place. And this is where we need to get a little more specific…

Regular spend versus manufactured spend.

Note that Ben didn’t talk about using the 2% threshold for credit card spend in general, but rather for manufactured spend. There’s a reason for that. We all spend money, of course. There’s not much choice in the matter. The only choice we have is what form of currency to use — cash, credit cards, Bitcoins, gold, frankincense, myrrh, or even old fashioned bartering with goods. Though for the record, you do not get anywhere near as many rewards points when conducting your transactions using chickens as your currency of choice.

The point is that we don’t really have the option to sit on our butts when spending money in the normal course of living our lives. We’re going to have to spend some money somehow.

Of course, credit cards aren’t always dandy either. Studies show that people using credit cards tend to spend more than those using cash, even when they’re responsible users who pay their bills in full. That’s why retailers are willing to pay 2% to 3% in transaction fees to accept credit cards, because they expect greater sales in return.

However, if we’ve made the decision to use credit cards to get rewards, then 2% is a valid baseline to measure all other rewards against, and if we choose to do it with anything less than a 2% cash back card we’re leaving rewards on the table. But…

What about money we don’t have to spend?

Manufactured spending is a somewhat different beast. We don’t have to spend that money. In fact, if we’re doing it correctly, we’re not actually spending it at all. So even if we make less than a 2% return, isn’t any return better than nothing?

On the one hand, there’s something to be said for trying to maximize your return on investment, and “investment” includes time and effort as well as money. On the other hand, if you set up a lemonade stand and decided to charge 50 cents per cup instead of 75 cents, and therefore you ended up with a profit of $50 for the day instead of $75, I don’t think it’s fair to say you lost $25. You put in a day’s work and got $50 in return for it. It’s not as good as $75, but you’re still ahead of the game compared to not doing it at all.

Of course, manufactured spend still involves paying fees, and those need to be figured into your calculations no matter what you’re earning in return. Too many folks dismiss those fees as trivial, but they add up faster than you realize. Even a $4.95 fee on a $500 gift card is chewing up practically half of the 2% return you’d get from buying that gift card with a cash back card. That’s why it’s important to find as many ways to minimize and offset those fees as possible.

Is the Devil’s Advocate arguing a distinction without a difference?

Some folks are going to tell me I’m full of it this week and don’t know what I’m talking about. Actually, some folks tell me that every week, along with making suggestions about my lack of intelligence and my personal hygiene habits. That’s one of the aspects of Twitter I’m a little less fond of.

But I have to admit I’m not terribly convinced by my own argument this time around. I do think when you’re manufacturing spend, any net return you get (above and beyond the fees you paid) is a positive. As long as you think it’s worth your time to get that return, why not go for it?

However, manufactured spend also requires a great deal of organization and if you’re already putting that kind of effort into it, it’s probably not that much harder to also make sure you’re maximizing your rewards for doing it. So if you’re collecting points at 1x via manufactured spend and those points aren’t worth at least 2 cents each, it’d probably be worthwhile to question exactly what you’re doing and whether you should adjust your plan.

To me, the biggest issue is determining exactly what a rewards point is worth in the first place. There’s a wide variety of opinions on the value of every loyalty currency, and while you might think a Starwood point is worth 2.1 cents, another person might say it’s worth only 1.8 cents. Only cash has an absolute value — the rest is educated guessing.

But making those types of determinations is part of the game we play, so set your priorities, pick your currency, and then don’t worry about what anyone else thinks. Especially not some guy who’s already on his 4th glass of Step Three.

Devil’s Advocate is a bi-weekly series that deliberately argues a contrarian view on travel and loyalty programs. Sometimes the Devil’s Advocate truly believes in the counterargument. Other times he takes the opposing position just to see if the original argument holds water. But his main objective is to engage in friendly debate with the miles and points community to determine if today’s conventional wisdom is valid. You can suggest future topics by following him on Twitter @dvlsadvcate or sending an e-mail to dvlsadvcate@gmail.com.Recent Posts by the Devil’s Advocate:

- Can We Find Anything Redeeming About Plenti?

- People Lied, Redbird Died! So Who Do We Get To Blame?

- Is the New 30% Rebate on Amex Pay With Points Better Than We Think?

Find the entire collection of Devil’s Advocate posts here.